Your Pension Promise is 110% Secure

CAAT Pension Plan Publication

Your Pension Plan delivers benefit security for members, with a 110% funding level.

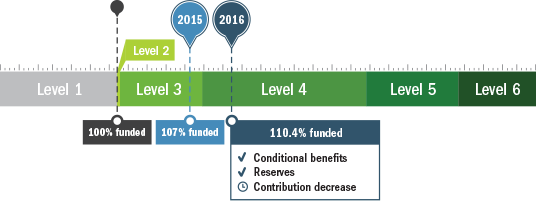

Results of the January 1, 2016 actuarial valuation, which will be filed with the regulators, show the Plan is 110.4% funded, (up from 107.2% in 2015). That means that for every dollar of pension promised to members, the Plan has $1.10 dedicated to stand behind it.

The Plan’s reserves have increased to $1.2 billion (up from $773 million in 2015).

What is an actuarial valuation?

The actuarial valuation compares the Plan’s liabilities – the pensions earned by members, and the estimated pensions that will be earned in the future – to the assets of the pension fund and estimated contributions to be received.

When the value of the fund, and the value of the liabilities match, the Plan is 100% funded. When the Plan is more than 100% funded, it means the Plan has additional reserves backing the promised pensions.

How did we get here?

The Plan’s ongoing stability is the result of strong investment performance and setting contribution rates at a level that reflects the desire for a secure and sustainable pension plan. These factors have been built on the solid foundations of joint sponsorship, prudent and realistic assumptions, and a well-thought out funding policy. This valuation demonstrates the Plan’s progress in meeting the goals of providing benefit security at stable and appropriate contribution rates. As a result of the Plan’s 110% funded status:

- Conditional inflation protection (on service after 2007) will be paid on pensions in payment until at least 2019.

- Contribution rates can remain stable, until at least 2020.

The next required valuation is not due to be filed with the regulator until January 1, 2019. The Plan’s 2015 investment results will be released in April, and further details will be included in the 2015 Annual Report which will be available in May.

What benefits does the Plan provide?

- Lifetime pension, with flexible start dates

- You can start your pension any time from age 55, (or as early as age 50 if you have at least 20 years of service in the Plan) and your pension will be paid for the rest of your life

- An expected 800% return on your contributions

- The average member who retired from the Plan has received approximately 8 times their contributions back in pension payments over their lifetime.

- Additional benefits add even more value

- Inflation protection increases help protect the buying power of your pension

- Survivor benefits protect your eligible spouse

Key assumptions that affect the valuation results

The actuarial valuation must take into account economic and demographic realities to ensure that risk is properly measured and managed.

Discount rate

Retirement age

Asset smoothing

Plan enters Level 4 of Funding Policy

As a result of the January 1, 2016 actuarial valuation, the Plan now sits inside Level 4 on the Funding Policy. Plan governors decided to retain the Plan’s surplus identified in this valuation as a reserve, consistent with the desire for benefit security and contribution stability as outlined in the Funding Policy. As the Plan moves further into Level 4, governors will reassess the options outlined in the Funding Policy.

The Funding Policy is one of the key tools used by Plan governors to ensure benefit security and stable contribution rates. There are three funding controls: reserves, contributions and conditional benefits. Each control has specific application based on the Funding Level of the Plan.

A going-concern valuation assumes the Plan will continue indefinitely and is used to measure whether contribution rates are sufficient to keep the Plan fully funded in the long term. A valuation must be filed in accordance with pension law in Ontario and meet the standards of the actuarial profession. The Plan is 110.4% funded on a going-concern basis, which means it is within funding Level 4 of the Funding Policy.

The solvency valuation shows the status of the Plan as if it had been wound up on the valuation date. For jointly sponsored plans like ours, the results are hypothetical only, as we are not required to fund for solvency deficiencies reflecting the ultra-low probability of the cessation of all participating employers at once and, instead, base funding requirements on the going-concern valuation. The solvency status is for disclosure purposes only. The Plan’s solvency position as of the January 1, 2016 valuation shows a deficit of $2.1 billion and a solvency ratio of 0.80.

Full story and others at https://www.caatpension.on.ca/en/newsletter/member-newsletter-march-2016.